The National Business Review reported a comment by New Zealand’s then National Party government Minister of Finance, Bill English, on Aug. 15, 2014, that he had occasionally pointed out in speeches to business audiences that New Zealand has had post-World War II recessions roughly every ten years: in 1957-58; 1967-68; the mid-1970s; the mid-1980s; 1997-98 and 2007-8. He would observe laconically: “You’d think we would see them coming.”

But, of course, bourgeois economists, commentators, and journalists don’t generally see them coming. One problem, however, is that sometimes the Marxist critics of capitalism see them coming a little too often.

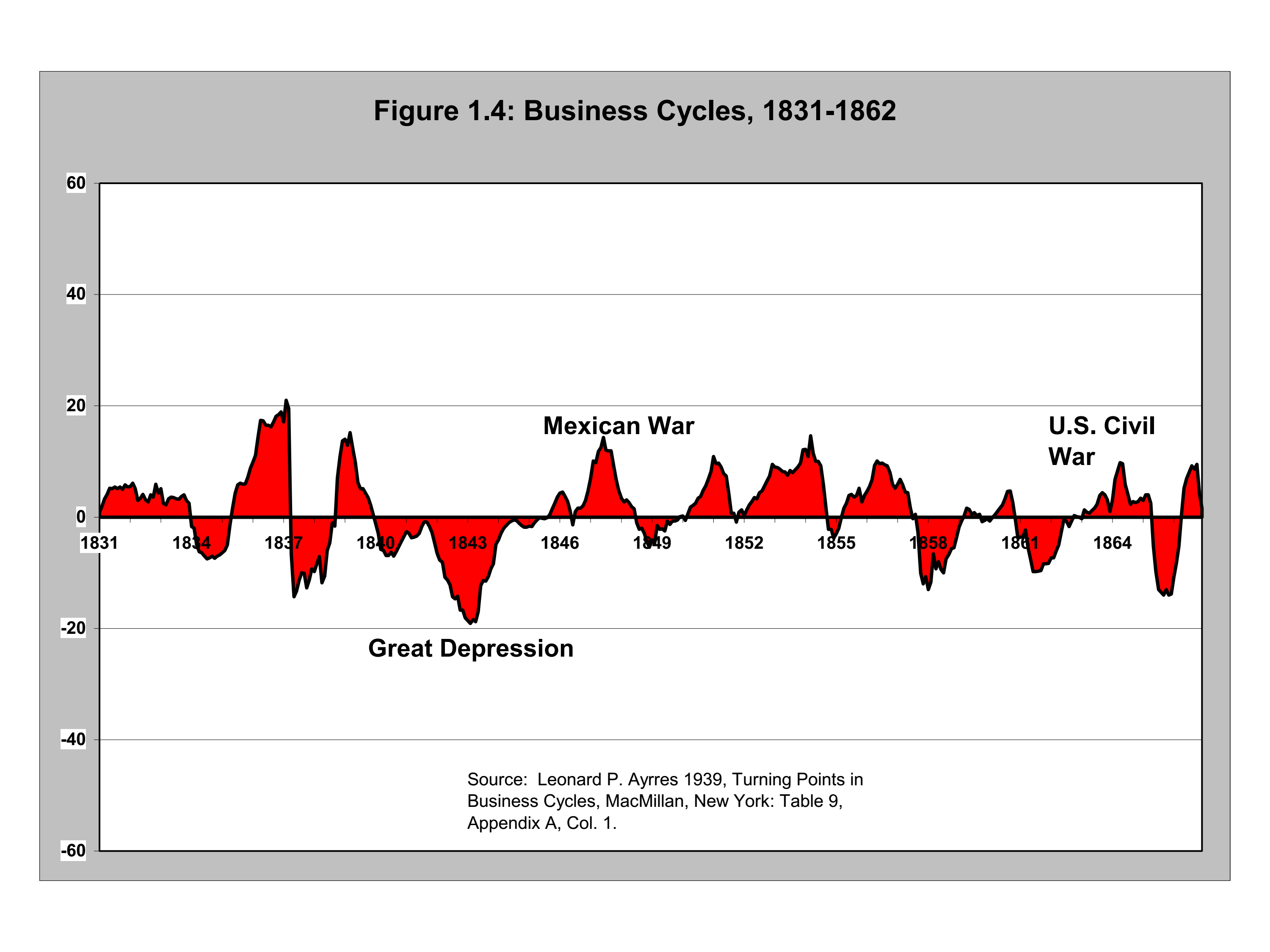

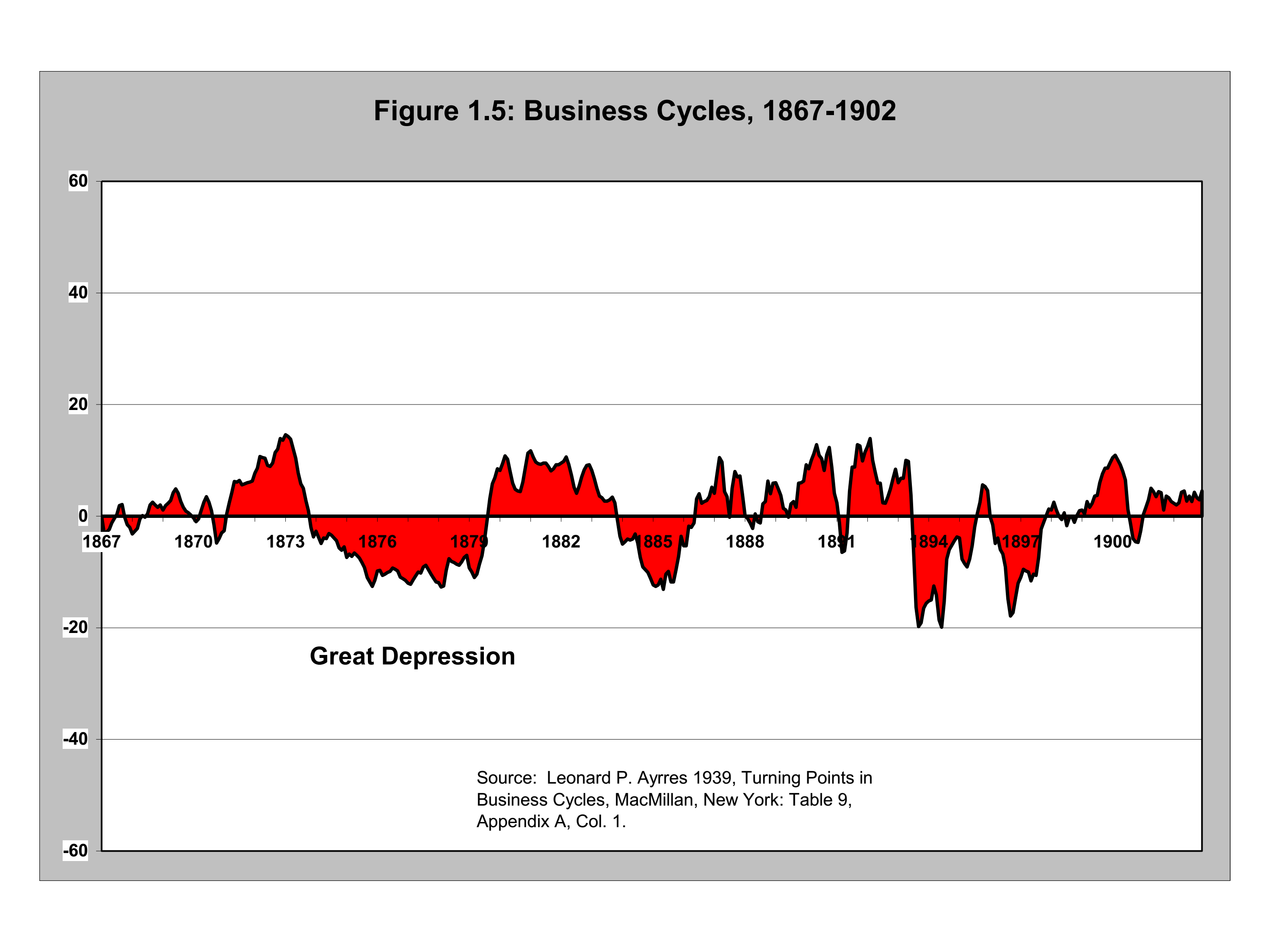

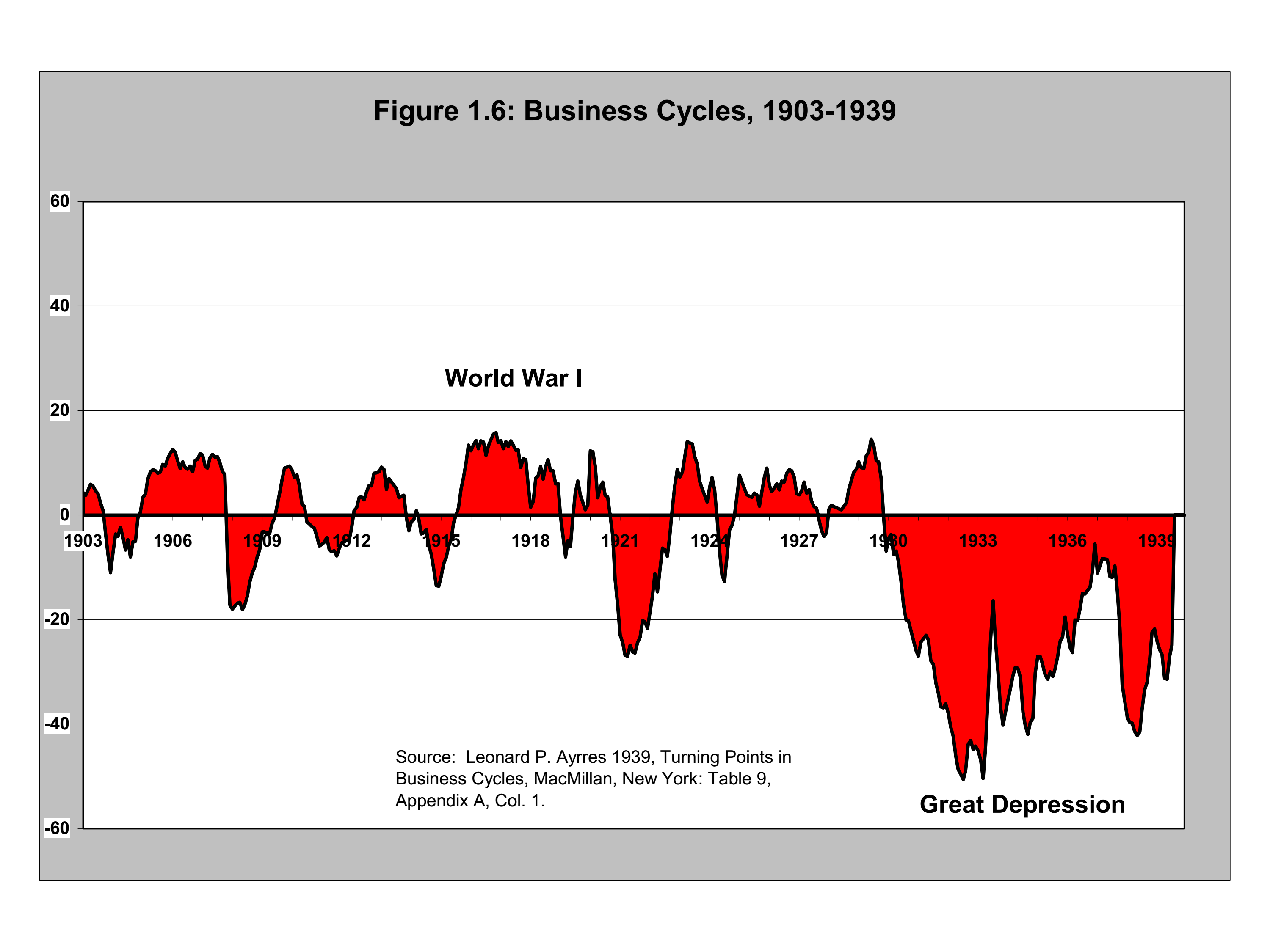

But it is a simple fact of life that capitalism has had economic crises on a periodic basis, at least since 1825. Every 10 years or so, capitalism goes through a cycle of boom and bust. The following charts for the U.S. economy illustrate this reality. They were taken from an important paper by U.S. Marxist economist Anwar Shaikh entitled: “Profitability, Long Waves and the Recurrence of General Crises.”

Capitalism also goes through historical periods where the industrial cycles of boom and bust are more pronounced one way or another. That is, capitalism goes through periods of several decades, such as the post-World War II “long boom” involving multiple cycles where the upturns are relatively stronger than the downturns.

Similarly, there are other periods, such as the decades following the crisis of 1873, where the upward phases of the cycle are relatively weak and the downward phases more pronounced.

Understanding these cyclical fluctuations is also closely connected to another element of Marxist theory that is important to explain what is happening — historical materialism — which is simply a way of viewing and understanding history.

Ever since we humans began generating a consistent surplus, societies have been divided into classes where each class is defined by its relationship to the means and mode of production. The legal, political, social and cultural elements of society arise from this economic foundation.

The relations and modes of production, which determine how the economic system is produced and reproduced, have gone through various stages as technology and the forces of production have advanced. The main stages have been slavery, feudalism, capitalism and the beginning efforts to construct socialism.

Economic systems do not pass away until they have exhausted their progressive functions in terms of increasing society’s productive capacity, which in turn enables population growth and cultural development. When the growth of the productive forces reaches a certain limit within the framework of the existing society, the question is posed: Can the fetters of the existing social relations be thrown off and a new society established?

Marx’s answers

Karl Marx devoted his life to answering this question in relation to capitalism. This was the question from his point of view. Decades of research, decades of writing, decades of reflection — in between throwing himself into labor struggles and the odd revolution when they were happening. But he always returned to this basic task.

The key questions were understanding why capitalism operates the way it does and whether capitalism is a historically limited system — whether it will reach a limit and need to be superseded. Marx’s answers are to be found in his writings, especially his great work known as Capital.

Our inability, so far, to supersede capitalism on a world scale means that periodic crises return, again and again, each one causing great hardship while giving a powerful impetus to the centralization of capital and the growth of monopoly domination.

The system’s dependence on relentless expansion over time and its inherent drive to maximize profit rather than meet human needs mean that we now face the incompatibility of this system with our coexistence with Mother Earth.

That has become an element of crisis theory in the broader sense — demonstrating the increasing incompatibility between a livable environment and the way the system is organized through private property and ownership.

The crises, therefore, tend to get bigger, more prolonged, and more socially destabilizing. We have entered a new period like that with the 2007-8 world recession, the weak recovery following, and now the post-COVID boom and bust in rapid succession.

But there is no final crisis in this system — other than a descent into nuclear war or barbarism arising from the sort of ecological winter or runaway ecological collapse that capitalism appears to be preparing for us. Short of such a disastrous outcome, the system will continue to carry on with its booms and busts until it is overthrown and replaced.

That can only be carried out by a conscious social and political force, by a class that is not bound to the system by material interest. That is why the working class is the only class that can overthrow this system. It is the only class not bound by property and profit to its perpetuation. It is the only class with the numbers and social power, if organized, if conscious enough, to effect this outcome and bring about real majority rule.

Marx’s challenge

The problem faced by Marx was that the challenge he took on in his writing of Capital was so daunting that all we got during his lifetime was the first part of a planned six-part work.

Marx published volume 1, part of his planned first volume in several editions. Friedrich Engels, using Marx’s notebooks, produced what we know of as volumes 2 and 3 after Marx’s death. Then there was the Theories of Surplus Value — a part of a rough draft of a history of economic thought. All of that was originally going to be the first volume of the planned six-part project.

There were to be additional volumes on wage labor, the state, and competition. The entire work was to culminate in the volume on the world market. It was there logically that crises were to be dealt with in a systematic way. Marx does not deal with crises except in scattered references, mostly in volume 3 of Capital and in his correspondence.

Marx’s method was to begin at the most abstract level before moving progressively to the more concrete. In Capital, he begins with the abstract categories of the commodity and value and moves through to the formation of prices and the role of money and the market.

He goes on to explain the origin of profit in surplus value and ties this all in with the origin of capitalism in what he called “primitive accumulation.” Systematic treatment of things like exchange rates, world trade, and so on was to come later.

There was an added problem with what we know as volume 2, published after Marx’s death. Volume 2 is actually more a volume about how capitalism works rather than how it doesn’t. Marx explains how capitalism must be a system of expanded reproduction, and he presents formulas to prove that is how it must exist and, in a sense, how it can exist.

There was a certain consternation and debate inside the socialist movement when volume 2 was published. The revolutionary ideas of Marx and Engels were already under attack within German Social Democracy, the German workers’ party at the time, which followers of Marx and Engels led. Volume 2 was used by critics of these revolutionary ideas to “prove” that capitalism worked and could last indefinitely — in support of the views of the reformist wing of German Social Democracy led by Eduard Bernstein.

Because the cause of crises wasn’t fully spelled out in Marx and Engels’ work, revolutionaries like Rosa Luxemburg started to look for explanations for why crises happen that didn’t quite fit in with the logic of what Marx and Engels had written. She looked at the exhaustion of the world market. Others looked at things like the tendency of the rate of profit to fall, which Marx viewed as a long-term historical tendency.

This logic can be deduced from their major economic works and their journalism and correspondence in which they wrote about and analyzed actual crises until Marx’s death in 1883 and Engels’ in 1895.

Capitalism has also changed significantly since Marx and Engels wrote. These changes need to be incorporated into our understanding of crises. The system has evolved from industrial capitalism based on free competition to monopoly capitalism.

We have been through the Great Depression of the 1930s. We have had the experience of the “Keynesian revolution.” We have had the Monetarist counter-revolution inspired by U.S. economist Milton Freidman and the debates in economic theory around that.

We have also had an end of the international gold standard, a very important event. We had the stagflation of the 1970s and the neoliberal turn in the 1980s.

Most recently, we have had the global “Great Recession” of 2007-9, followed by an unprecedentedly weak recovery, anemic at best for most of the world. Monetarism appeared to be abandoned briefly in favor of Keynesianism again to confront the COVID-19 crisis, only to be reimposed to crush the inflation unleashed in its wake.

Today we are facing a renewed global recession that threatens a return of a great depression. This is because the weak recovery after 2008 still required an enormous explosion of debt. The inflationary money printing followed this to cope with the COVID-19 crisis that will require interest rates we haven’t seen in decades to bring under control. That, in turn, will provoke a cascade of debt and broader financial crises across the globe.

Conflicting crisis theories

Marx had identified the essence of the periodic crises of capitalism as crises of overproduction very early on, even in the Communist Manifesto in 1848. This crisis can only happen because production periodically exceeds monetarily effective demand, which is ultimately determined by the existing size and growth rate of the global hoard of the money commodity — gold.

I am emphasizing this because there has been a retreat from this analysis, including among followers of Marx. In fact, the two main schools of Marxist crisis theory today are not schools based on periodic overproduction crises.

One school is based around the primacy of the tendency of the rate of profit to fall (TROPF). Marx introduced this idea in volume 3 of Capital as an important long-term historical tendency in capitalism. Marx also pointed out many counter tendencies, but the tendency is true over long periods. Many Marxist economists use that important theory as the primary explanation for why capitalism has crises.

This school of thought is associated with the U.S. academic Andrew Kliman and British theorists from the Trotskyist tradition, including the British Socialist Workers Party (SWP) leader Alex Callinicos and the prolific blogger Michael Roberts. All three writers deserve to be read, and there is much to learn from their writings.

But the almost monomaniacal attachment to the TROPF to explain crises leads them astray.

Michael Roberts even tries to explain the 10-year cycle under capitalism as a result of the fall in the rate of profit. It is, of course, true that every crisis is associated with a fall in the rate of profit, but that temporary decline is a result of the crisis, not the cause.

Callinicos seems unable to explain the real growth of capitalism since the 1980s. Because the early 1980s crisis must have been the result of the TROPF, and since there has been no counter tendency big enough to overcome the falling rate of profit sufficiently, the crisis must be permanent. However, the world economy has more than doubled in size in that period, and we have seen an explosive growth in capitalist production in China, which he fails to properly account for in his theories.

The other significant school of thought is associated with the U.S. Monthly Review magazine and its editor John Bellamy Foster. Foster is an important writer on economic matters for the magazine and a leading theorist on Marxism’s relevance to understanding today’s ecological challenges. The Monthly Review school is very influenced by Keynesian ideas. John Maynard Keynes was a pro-capitalist economist who became very influential in the wake of the Great Depression of the 1930s.

Traditional bourgeois economic theory denied that capitalism could have crises. Keynes had been schooled in this theory but, when faced with the crisis of the 1930s, was forced to acknowledge the reality staring him in the face. This was that capitalism could have crises; in fact, it seemed to him to have a tendency towards stagnation. But he believed the state could intervene to alleviate crises, if not eliminate them altogether.

So from a Keynesian point of view, you cannot have a crisis of overproduction. Rather, with Keynes, you have a crisis of under-consumption that can be resolved by the state stepping in to purchase goods directly or printing money to give people to spend themselves and/or using government deficit spending to put more money into the economy. Part of the reason Keynes favored ending the gold standard was to allow this to happen more easily.

Overproduction as the underlying cause of crisis, which is based on Marx’s concept of money as the universal equivalent, has been — especially since the end of what remained of the international gold standard in 1971 — all but forgotten, including by most of those claiming to be Marxist.

Capitalism requires a measure of value that is itself a commodity

Classical political economy, represented by Adam Smith and David Ricardo, was the science of capitalism. Marx developed and perfected their labor theory of value. Smith’s “invisible hand” — the unobservable market force that helps the demand and supply of goods in a free market to reach equilibrium automatically — was the law of labor value in operation.

But Marx also explained that what Smith and Ricardo called “labor” was actually “labor power” or the ability to work. But a capitalist won’t employ labor unless the worker can produce more value in a workday than what they are paid. This “surplus value” is the origin of all forms of profit and drives the invisible hand. This made Marx’s ideas a revolutionary advance on classical political economy and forced the capitalists to abandon the science of political economy.

A central part of Marx’s perfected labor theory of value was that it requires — as does commodity production as a system — a measure of value that is itself a commodity.

Ultimately, gold emerged as the main money commodity because it is durable, contains significant value (amount of abstract human labor measured in units of time) in a small quantity, and is easily divisible. However, it can only be a measure of value because it has value as a product of labor itself, measured by its monetary use value in units of weight.

The pro-capitalist alternative to that theory and Keynesian under-consumptionism is dubbed Say’s Law — an economic principle of early “vulgar” economics named after the French businessman and economist Jean-Baptiste Say (1767—1832). Marx dubbed them “vulgar” economists because they had ceased to seek a scientific explanation for what was happening and instead provided simple apologies for capitalism and its laws.

Say stated that production creates its own demand. Commodities are bought with commodities. Money plays no particular role except as an intermediary.

This idea, combined with marginalism — the theory that commodities have exchange value because of their scarcity relative to human needs — tries to banish the labor theory of value by claiming things have value due to their marginal utility and that generalized overproduction of commodities is impossible.

Essentially, this is a subjective rather than objective theory of value. Marginalism, which assumes Say’s Law either explicitly or implicitly, was the end of bourgeois economics as any form of science. All bourgeois economics today is built on these two theories and can’t escape them.

The abolition of the gold standard has created very real problems with the modern U.S. dollar-based international monetary system, with permanent inflation, regular exchange rate crises, and so on. Following the Bretton Woods monetary conference in 1944 up to 1971, when Nixon took the dollar off the gold standard, money in everyday use nearly always had a legally fixed relationship to gold via the U.S. dollar.

You could go to a central bank and demand a certain amount of dollars for your currency, which in turn would represent a specific amount of gold-backed by the bullion hoard in Fort Knox.

Prior to 1933, individuals, as well as countries, could demand gold for their paper U.S. dollars. After 1933, up to 1971, foreign governments and their central banks — but not individuals — could do the same.

But after the gold standard was completely abandoned, there was an assumption on the part of many Marxist economists that maybe Keynes was right on one point. Maybe now you could just create money at will. The state had the power not just to create tokens representing gold but create currency at will with no relationship to gold — now supposedly “just another commodity” like all others with no special role.

That is a big mistake. Ultimately, all non-commodity money — token money and credit money — must have a relationship to a real money commodity like gold. This is true whether a formal gold standard exists or not. This lawful economic relationship still exists and therefore continues to be the underlying cause of crises of overproduction.

When they started to print money at will, in the 1970s, when Nixon said, “We are all Keynesians now,” you ended up with a severe bout of inflation as printed money lost value and its fixed relationship to the money commodity, which remained gold.

The “price” of gold surged — it took more and more tokens to represent the same amount of gold. Monetary tokens were being devalued, and inflation was the inevitable result.

Engels (and Marx) on overproduction crises

The nature of a crisis as an overproduction crisis was spelled out by Engels in 1873.

Engels was a remarkable man. He worked managing his family business in Manchester for some decades, operating as a capitalist in the textile trade. He did that so he could keep his friend and intellectual partner free to work on Capital. He hated what he did.

Engels was a brilliant man, but he knew there was one person — Karl Marx — who alone at that time was both willing and able to carry through the critique of bourgeois political economy. Engels was willing to do whatever was necessary to enable Marx to work. The correspondence of Marx and Engels is extraordinarily rich in political and economic analysis.

Engels begged Marx to get on with the task of writing the book. Marx promised again and again that it was just around the corner. There came a certain point in his life when Engels could give the business up, and there is a wonderful letter where he expressed his joy at being liberated from his role as an industrial capitalist.

Engels did a lot of writing in defense of the joint views of Marx and Engels. One of his major works was a polemical work in 1877 called Anti-Duhring against a then fashionable but now obscure German professor. It became an exposition of the mature views of Marx and Engels on a broad range of political, historical, philosophical and economic ideas.

By this time, all of Marx’s major economic concepts had been developed. He even wrote a chapter of Anti-Duhring himself. For those attached to the TROPF, it is not mentioned once as a cause of crisis. However, they did write an important paragraph summarizing their joint views on the origin of crises under capitalism. It reads:

We have seen that the ever-increasing perfectibility of modern machinery is, by the anarchy of social production, turned into a compulsory law that forces the individual industrial capitalist always to improve his machinery, always to increase its productive force.

The bare possibility of extending the field of production is transformed for him into a similarly compulsory law.

The enormous expansive force of modern industry, compared with which that of gases is mere child’s play, appears to us now as a necessity for expansion, both qualitative and quantitative, that laughs at all resistance.

Such resistance is offered by consumption, by sales, by the markets for the products of modern industry.

But the capacity for extension, extensive and intensive, of the markets, is primarily governed by quite different laws that work much less energetically. [Emphasis added]

The extension of the markets cannot keep pace with the extension of production.

The collision becomes inevitable, and as this cannot produce any real solution so long as it does not break in pieces the capitalist mode of production, the collisions become periodic.

Capitalist production has begotten another “vicious circle.”

The problem is Engels didn’t spell out what these laws are that govern the capacity for growth of the markets and why they work much less energetically.

But he spells out that he sees the cycles of capitalism and the crises they produce as a periodic collision of two counterposed forces—the physical ability of capitalism to use modern science and technology to expand production without limit, and the different, less energetic laws governing the growth of the markets.

Laws governing the growth of markets

The laws that govern the growth of markets are connected to the role of the money commodity as a measure of value and periodic changes in the relative profitability of gold production versus the production of other commodities.

Gold is both the universal equivalent, the measure of value, and a commodity in its own right. Therefore its production remains key to understanding the laws of capitalism that determine value, price and profit.

But if you look at the history of capitalism, there is a peculiarity about gold. Because it is the ultimate measure of value, the production of gold tends to move countercyclically to overall commodity production. So when there is an overall boom in production in society, gold production tends to decline, and during overall depressions in society, gold production tends to increase. This is an important mechanism for regulating capitalism.

As prices in gold terms (in weights of gold) rise during the rising phase of the industrial cycle, gold’s purchasing power falls, gold production becomes relatively less profitable, and capital flows out of that sector, gold production slows, interest rates rise as money becomes tight, and the boom ends in a crash.

When prices in gold terms fall sharply in a crisis, gold’s purchasing power rises, gold production becomes relatively more profitable, and capital flows into the sector, causing gold production to rise, adding to the growing idle money hoard resulting from the crisis itself, pushing down interest rates, and the economy recovers.

The capitalist system seeks to escape the limits of monetarily effective demand by, as Marx explained some 150 years ago, expanding credit. But credit cannot expand forever, even with all the modern-day miracles performed by modern computers. In the end, the debt must be serviced—interest and principal paid—and eventually the game is up. Interest rates rise during the industrial cycle’s boom (overproduction) phase, credit collapses, and another crisis is born.

Critique of Crisis Theory blog

In the last decade, I have been working with a small group of Marxists in North America doing a blog focused on economics that I highly recommend. It is called A Critique of Crisis Theory. What I have been explaining here are essentially their ideas.

The blog’s first 40 or so posts are being turned into the draft of a book we hope to serialize soon. The author of the blog, Sam Williams, and his collaborators have been working on their economic ideas for some decades. The creation of the Internet has allowed these ideas to be shared with a much wider audience than was possible before.

More recently, Williams has been responding to new developments and discussing with others who have engaged or critiqued his ideas. I tried to critique his views on an aspect of economic theory I thought I had some familiarity with — productive and unproductive labor.

Classical economists and Marx recognized that not all labor performed was productive of value and surplus value. We can see this easily when we look at the “labor” of a police officer, priest or soldier versus the labor of a miner or factory worker. I think we can identify who is a productive worker in that picture.

It gets more complicated when we look at the labor of bank workers and retail workers whose labor may or may not be necessary for production to occur. It gets even more complicated when we look at workers in health and education who may be employed in a private business producing a profit for the capitalist. Anyway, that is the area I wanted to discuss.

Sam was patient in his responses and took the time to respond to my first questions in a very pedagogical way.

Then when I wrote back, still disagreeing, he wrote an even longer and more thorough response that included a reference to Albert Einstein, who, he said, proved that matter and energy are different forms of the same thing, just as physical goods and “non-material” services can both be commodities embodying labor value. That sealed the issue for me, and I conceded they had a far better understanding of this issue.

What I found by following the blog was that it appeared to answer many of the questions and doubts I had from my own reading of Marxist economic theory, which has been an interest of mine though I am no “expert,” which I will come back to. From a young age, I had been very interested in Marxist economic theory. Initially, I had been strongly influenced by a prominent Belgian Marxist economist named Ernest Mandel. Much of what he wrote remains useful.

In some things he wrote in the 1970s, Mandel hints at the continuing importance of the role of gold as the money commodity. He played an important role in analyzing the “long waves” of 40 or 50 years duration that appear to be a feature of capitalism, which I believe is correct.

The Critique blog author also believes long waves play an important role and provides an explanation for a long cycle based on long-term swings in gold production, which makes the argument for its importance even more powerful.

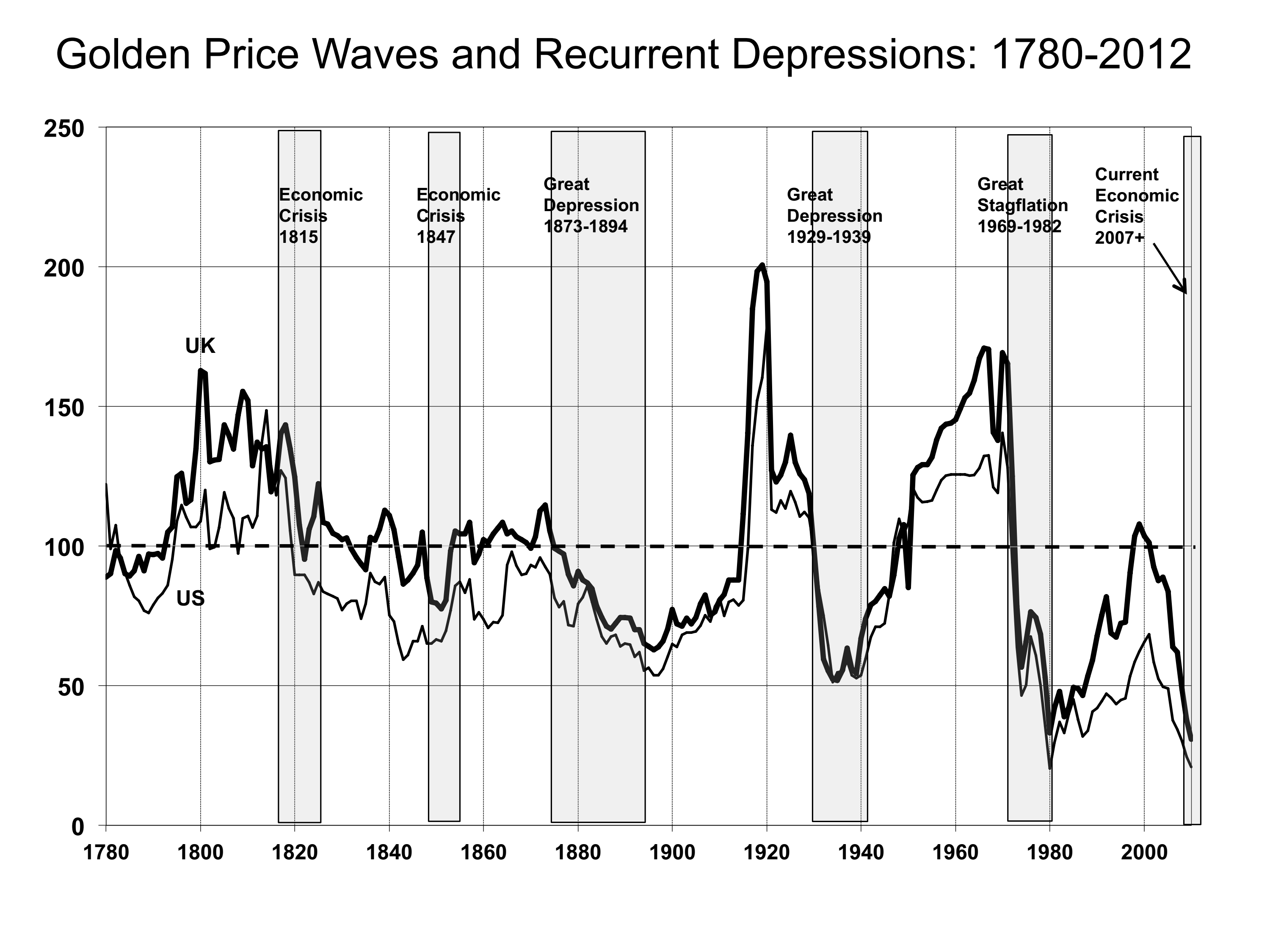

Another fine economist, Anwar Shaikh, who knows his Marx and supports an understanding of the history of capitalism involving long waves, has produced a graph that seems to support the Critique of Crisis theory on this point. He follows the long-term movement of wholesale prices in the U.S. and the UK.

He shows in his graph that there is a movement in wholesale prices upwards during a period of the long wave that is dominated by strong upturns in the business cycles and trends downward in prices during a period of the long wave where business cycles are dominated by the downward phase of the cycle. The decline in wholesale prices is associated with a period of stagnation or long depression under capitalism. So we have the 1873-1893 decline, the Great Depression of 1929-1939, the Great Stagflation of 1967-1982, and a similar decline, which he argues indicates a new Great Depression, beginning in 2008, which he describes in a lecture as a “very scary” conclusion for his students at that time.

To produce an accurate version of the graph, he needed to measure the prices in terms of gold because, in the period following the abolition of the gold standard, there has been a permanent inflation in paper money prices that hides the real movement of prices in gold terms. This fits very closely with the Critique of Crisis Theory blog’s view, even though Shaikh is broadly in the school that looks for the cause of crises in the TROPF.

The crisis theory blog brings the very useful empirical work by Shaikh into long waves and crisis theory together in a blog as follows:

As a rule, after several industrial cycles dominated by the boom phases, the general price level rises above the value of commodities. This causes the rate of profit in the gold (money material) producing industries — mining and refining — to become less profitable than most other branches of industrial production. Capital, therefore, begins to flow out of gold production and refining.

As the production of money material declines, the quantity of money grows at an increasingly slow rate relative to real capital — productive and commodity capital. As a result, credit increasingly replaces money, eventually stretching the credit system to its limits.

Money becomes tight, and interest rates rise. This situation, assuming capitalist production is retained, can only be resolved by a crash or a series of crises and associated depressions of greater than average intensity, duration, or both.

One result of a crisis or series of crises of greater than usual violence or duration is a lowering of the general price level — measured in terms of the use value of gold bullion — once again to below the value of commodities. This makes gold production and refining industries more profitable than most other industries.

Capital once again flows into gold mining and refining, causing the production of gold bullion to rise once again. The quantity of money then expands with low interest rates and “easy money.”

As the process of liquidating the previous overproduction goes on, especially of those commodities that serve as means of production, the accumulation of (real) capital stagnates. As a result, for a period of time, money capital is accumulated at a faster rate than real capital.

But once the accumulated overproduction — especially in the form of surplus productive capacity — is liquidated, a new “sudden expansion of the market” occurs, leading to a series of industrial cycles dominated by the boom phases rather than the crisis or depression phases.

This “long cycle” is built into the commodity foundation of capitalist production and is the inevitable result of the commodity form itself once it is fully developed.

But this cycle is also affected by accidental events such as discoveries of rich new gold mines and technological improvements in gold mining or refining that can either weaken or reinforce it depending on circumstances, as well as by such “accidents” as wars and revolutions.

So history is not an automatic repetition of cycles but a complex process involving both chance and necessity.

Williams and his collaborators are quite orthodox in demanding a return to Marx on the nature of capitalist crises as crises of the general overproduction of commodities. At the same time, they incorporate major developments of the capitalist system in the 150 years since Marx and Engels wrote in order to explain what is happening today.

An important contribution

The Critique of Crisis Theory blog is making an important contribution to Marxist economic theory today. The blog is getting thousands of page views monthly and becoming influential in Marxist economic debates. It is getting the recognition and respect it deserves.

The world reality we face today is conforming to the central theses of the blog. The current unfolding crisis and the 2007-9 crisis are both clearly global crises of overproduction. There were simply too many houses, too many cars, and so on. Of course, “too many” from the point of view of being “too many” to be sold for a profit, not in terms of human need.

I think we all should pay respect to the founders of scientific socialism and give this issue of crisis theory the attention and importance it deserves. We cannot leave it to others, to “professionals” or self-selected “experts.”

I am not an “expert” on this stuff. It has been a continuing interest of mine because it is important that we understand it and because it is important we understand what is happening and who we are, what our role is, what we expect will happen to this system, who the agent of social change is going to be, and what the prospects are for making change in the world today. Those are all issues that anyone who wants to find a way out of the permanent crises capitalism seems to have in store for us can begin to address.

Mike Treen is an Advocate for Unite Union in New Zealand. Two decades ago, Unite began a successful campaign to organize workers who had lost union protection in the 1990s in an extreme “neoliberal” attack on workers’ rights. The employment law at that time did not mention unions. Unite now has union-negotiated collective agreements in fast food, cinemas, hotels and call centers. This includes at McDonalds, which hasn’t signed a collective agreement in any other country which has “voluntary” unionism and no legal compulsion to do so. In 2015, Unite Union led a campaign against zero-hour contracts in the fast food industry that led to their legal abolition under a National Party-led government. This party had implemented the 1990s reactionary anti-worker “reforms.” Unite Union is also active in broader social movements around migrant rights, housing and international solidarity movements like the struggle for Palestine. Mike Treen himself went on a boat trip to try and break the siege of Gaza in 2018. (See a 2009 report) or watch this video.)

Join the Struggle-La Lucha Telegram channel